Aldeman: 3 Differences Between California’s Teacher Pension System and Social Security That Have a Huge Impact on Retirees — New Report

;)

Untangle Your Mind!

Sign up for our free newsletter and start your day with in-depth reporting on the latest topics in education.

Teachers may not miss what isn’t there.

In California and 14 other states, plus the District of Columbia, public school teachers do not participate in Social Security. They won’t find any deductions for Social Security taxes on their pay stubs. Unlike teachers in other states who get both Social Security and a retirement plan, they are dependent solely on their state pension.

Avoiding taxes may seem like a good deal in the short term, but there are long-term risks, as nonparticipating teachers won’t get any Social Security benefits for their years of service. In effect, they are trading the safety and portability of the progressive Social Security benefit formula for the chance at a big payout from their state pension plan.

For certain types of workers, this might be a good trade. Under the California State Teachers’ Retirement System (CalSTRS), new teachers who start this year will eventually qualify for a pension equal to 2 percent times their years of service times the average of their highest three years of salary.

Critically, however, the salary used in the CalSTRS pension formula is not adjusted for inflation. That may not matter much for someone who’s already close to collecting benefits, but it matters a great deal for someone who’s far from retirement age. Every year a teacher has to wait to collect the pension is a year inflation takes a tiny bite.

The CalSTRS formula, like other teacher pension plans, provides benefits in a linear fashion. Workers who earn higher salaries while they work receive proportionately higher pensions when they’re retired.

Social Security works differently, in three key ways. First, and most obviously, Social Security is a national program. State pension plans do offer some features to allow for worker mobility, but those features have limits. Economists Robert Costrell and Michael Podgursky have found that teachers who move across state lines earn pensions worth 50 to 75 percent less than someone who stayed put.

Second, Social Security benefits are based on a worker’s highest 35 years of earnings, and all years are automatically adjusted for inflation. That protects people who may enter and exit the workforce at different points in their career, whether to take care of family or for other reasons.

But most importantly, Social Security is progressive. It was designed to provide disproportionately large benefits to lower-income workers. This stands in stark contrast to teacher pension plans like CalSTRS.

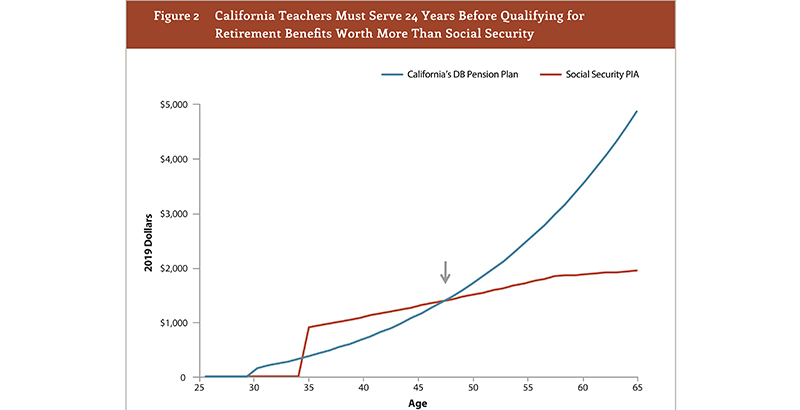

As I show in a new report for TeacherPensions.org, these three differences make a huge impact on workers. To illustrate what this looks like in real life, consider the case of a new teacher hired this year in California. She’s 25 years old. She makes $40,000. After 10 years of employment, she might be eligible for a monthly CalSTRS benefit worth about $730 when she retires. However, she’ll have to wait 27 more years to collect. In the meantime, the cost of groceries and health care and everything else will rise, while her pension benefit will not. By the time she’s eligible to retire, her pension will cover only about half of the value of what it would be worth today.

Now, imagine she had been participating in Social Security. Using the same assumptions, she would be eligible for a monthly benefit when she retires worth $890 in today’s dollars. But because Social Security benefits are adjusted for inflation, that amount will rise over time to cover changes in the cost of living.

As I show in my paper, this same teacher would need to teach for 24 consecutive years in California before she qualified for a CalSTRS pension benefit that equaled or exceeded the value of what she would have received under Social Security. This is the gamble California teachers — and educators in all the other non-Social Security states — are making. Pension plans like CalSTRS provide a much more generous benefit to those who remain teaching in one state for their entire career, but Social Security provides a better base level of benefits for everybody.

It wasn’t supposed to be this way. In the early 1990s, Congress directed the Internal Revenue Service to write a rule that would protect all state and local government employees who lack Social Security benefits. But, as my paper shows, that provision is not functioning as intended. Worse, the rule offers better protection for the highest-paid, longest-serving workers while leaving the most vulnerable employees short.

This situation is not trivial. In addition to 1.2 million active teachers who aren’t covered by Social Security, there are about 20 million retirees who performed some service to a state or local government without Social Security coverage. Many of those workers now face a lower standard of living in retirement due to the flaws in these seemingly arcane rules.

Workers may not even be aware of this problem, but Congress must act to fix it. After all, states on their own will never match the national portability provided by Social Security, and they have chosen not to match the progressive, inflation-adjusted benefits Social Security offers.

Chad Aldeman is a senior associate partner at Bellwether Education Partners and the editor of TeacherPensions.org. Bellwether was co-founded by Andy Rotherham, who sits on The 74’s board of directors.

Get stories like these delivered straight to your inbox. Sign up for The 74 Newsletter

Chad Aldeman is a regular columnist for The 74. He writes about school finance, state assessments and accountability, and the teacher labor market. He is also the founder of Read Not Guess, a program to help parents teach their children to read

@ChadAldeman